The Billion-Dollar Question: Who Controls the Proceeds of a Williamson Health Sale?

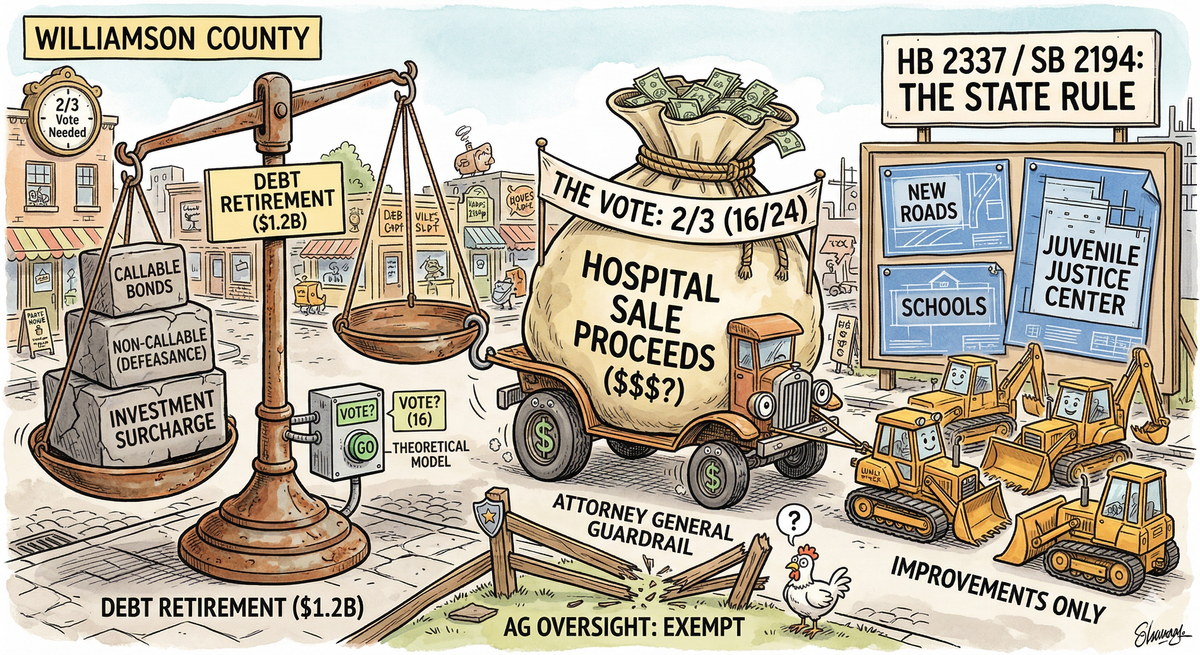

TN legislation (SB2194/HB2337) allows Williamson Co. to use hospital sale proceeds for "improvements" with a 2/3 vote. Comm. Lawrence notes that bond debt ($1.2B) can't be paid like a bill; it requires strategic calls or defeasance.

As Williamson County explores the potential sale of Williamson Health, much of the public conversation has focused on valuation, growth, and opportunity. But beneath those surface-level discussions lies a far more consequential issue—one that deserves far greater scrutiny: who controls the money once the sale is complete, and whether the law provides clarity—or simply discretion—on how it will be used.

At a recent County Commission meeting, Commissioner Gregg Lawrence described the potential sale as “the largest financial transaction in the history of the county.” That alone should shift the focus. This is not simply about selling a hospital; it is about what happens to a massive pool of public-benefit assets once they are converted into cash, and whether the rules governing that cash are clear enough to prevent conflict—or vague enough to invite it.

The Legal Framework and the "Guardrail" Problem

Under current Tennessee law, that question is not left open-ended. Tennessee Code Annotated § 48-68-206 places defined guardrails on how proceeds from the sale of a public benefit hospital are handled. The law requires that those funds remain tied to their original charitable purpose and assigns the Tennessee Attorney General a critical oversight role to ensure that standard is upheld.

That oversight includes evaluating whether the hospital is sold for fair market value, whether proceeds remain aligned with the original public trust, whether conflicts of interest exist, and notably, whether proceeds are improperly returned to local government. Under existing law, proceeds are generally not allowed to flow back into county coffers, except to satisfy lawful obligations. The intent is clear: prevent a public health asset from being converted into unrestricted government revenue.

However, the resolution passed by the Williamson County Commission—and the legislation currently moving through the General Assembly (SB 2194 / HB 2337) —seek to fundamentally change that structure. Presented by Representative Jake McCalmon (District 63) and State Senator Jack Johnson (District 28), the legislation effectively acts as a private act specifically for Williamson County. This shift moved forward locally when a resolution supporting these changes passed the County Commission with 17 of the 24 commissioners voting in favor.

Commissioner Lawrence: Debt Reduction and the Reality of Bonds

TruthWire News reached out to Commissioner Gregg Lawrence, who represents District 4 and was the sole commissioner on the resolution, regarding these proposed changes. Lawrence indicated that while he knows the language is written broadly, he feels there will be support from the commission for using the proceeds from the sale to at least partially pay down the county debt.

However, Lawrence clarified that the county's $1.2 billion debt cannot just be paid off like a regular monthly bill. Because the debt is through bonds that have a threshold for being able to legally call them in, there is an expectation of investment of those bonds that will provide a yield over time.

To understand why the county likely would not retire everything immediately, one must look at how these financial instruments work:

- Non-Callable Bonds: If a bond is non-callable, the county is legally obligated to keep paying interest until the maturity date. Bondholders bought them expecting that income stream, and the contract doesn't allow early redemption.

- Callable Bonds: Many bonds include a call provision that allows the county to redeem them before maturity, typically after a set call protection period (often 10 years). To call them, the county usually pays the outstanding principal plus any specified call premium.

- Advance Refunding / Defeasance: For non-callable bonds, a county can "retire" the debt through defeasance—placing sufficient funds (usually in U.S. Treasuries) into an escrow account to cover all future payments. This effectively neutralizes the debt, though the 2017 Tax Cuts and Jobs Act made this strategy more expensive.

Strategic Cash: The Juvenile Justice Center and "Improvements"

Critically, the legislation presented by Rep. McCalmon and Senator Johnson does not explicitly state that proceeds can be used for existing county debt. Instead, it specifies that the county can utilize proceeds, after debt service, for "improvements" such as schools, jails, or roads.

Because of the bond constraints, Commissioner Lawrence suggested that any projects or improvements needed can be paid for with cash instead of increasing the amount of debt. A primary example is the Juvenile Justice Center, which is one of the larger financial issues the county is currently navigating. By using sale proceeds to pay for this facility and other capital needs with cash, the county can avoid the interest costs of new bond issuances, effectively stopping the growth of the debt while managing existing obligations through a combination of waiting for call dates and exercising call provisions on callable bonds.

Theoretical Strategy: The "Clean Slate" Model

While the total proceeds from a potential hospital sale remain unknown, we can look at a theoretical model of what calling in as much debt as possible would look like. Based on the known $1.2 billion debt load, a total retirement strategy would involve two massive financial maneuvers.

First, the county would exercise every "Call Provision" currently eligible. This often requires paying a "Call Premium"—essentially a small penalty to bondholders for taking their high-yield investment away early. Second, for debt that is currently non-callable, the county would engage in defeasance.

In this theoretical scenario, the county would take a massive portion of the sale proceeds and place them into a "lockbox" of U.S. Treasuries. This escrow account would be mathematically timed to cover all future interest and principal payments. While the debt technically exists until the bonds reach their maturity dates, it is removed from the county’s balance sheet because the funds are already secured.

The "surcharge" for this strategy is the gap between the interest the county owes (often higher) and the interest the escrow earns (often lower). While this makes the immediate payoff cost higher than the face value of the debt, it theoretically saves the county from the $100 million annual interest drain that currently eats into the budget.

The 2/3 Majority Requirement: The Power of 16

The new legislation introduces a significant hurdle: any decision on how to use these proceeds must be approved by a two-thirds majority vote of the County Commission. In Williamson County’s 24-member body, this means 16 commissioners must agree on a specific spending plan.

This 2/3 requirement is a double-edged sword. It prevents a simple majority from making impulsive decisions, but it also creates the potential for a stalemate. To successfully execute the theoretical "Clean Slate" model or fund the Juvenile Justice Center with cash, a coalition of 16 members must align on a formal Debt Management and Capital Improvement Plan that:

- Prioritizes the redemption of callable bonds as they reach their call dates.

- Authorizes the "defeasance" of high-interest non-callable debt using escrow.

- Mandates that large-scale capital projects be cash-funded to prevent new debt.

Without this high bar of consensus, the funds could remain in a trust or be diverted to other "operational expenses" allowed under the broad language of the bill, leaving the $1.2 billion debt and its $100 million annual service costunchanged.

Conclusion: Accountability Relocated

This is no longer just a policy discussion; it is a question of whether the framework governing the proceeds provides sufficient clarity. As Rep. McCalmon stated, the bill allows the commission to decide on roads, schools, or jails—whatever they decide to vote on.

If the intent of the community is to ensure these proceeds are used to stabilize the county's financial footing, that outcome is not guaranteed by the law. It is only made possible by the law. The actual determination will come down to the votes of your local representatives.

As of late March 2026, HB 2337 and SB 2194 are nearing final passage. Once signed, the responsibility shifts to the local level. If you believe debt reduction or cash-funding future projects such as the Juvenile Justice Center should be the priority, now is the time to communicate with your County Commissioner to ensure they are part of the 16-vote supermajority required to secure the county's future.

If you want to support what we do, please consider donating a gift in order to sustain free, independent, and TRULY CONSERVATIVE media that is focused on Middle Tennessee and BEYOND!